MI member Argus provides its most recent global methanol industry view on pricing, supply and demand. Argus delivers a comprehensive view on global methanol markets, from upstream natural gas, coal, and other feedstocks to the downstream end user. They provide contract and spot prices, global industry news, analysis of key market drivers, price forecasts, supply and demand outlooks, and consulting. The Methanol Institute also provides low-carbon methanol pricing insights, available exclusively to MI members, offering visibility into emerging renewable methanol markets.

The Methanol Institute is sharing the information provided by Argus as a service to the community. This does not represent an endorsement by MI and we assume no liability whatsoever concerning the accuracy and completeness of the information presented below and disclaim all liability arising out of the use of such data.

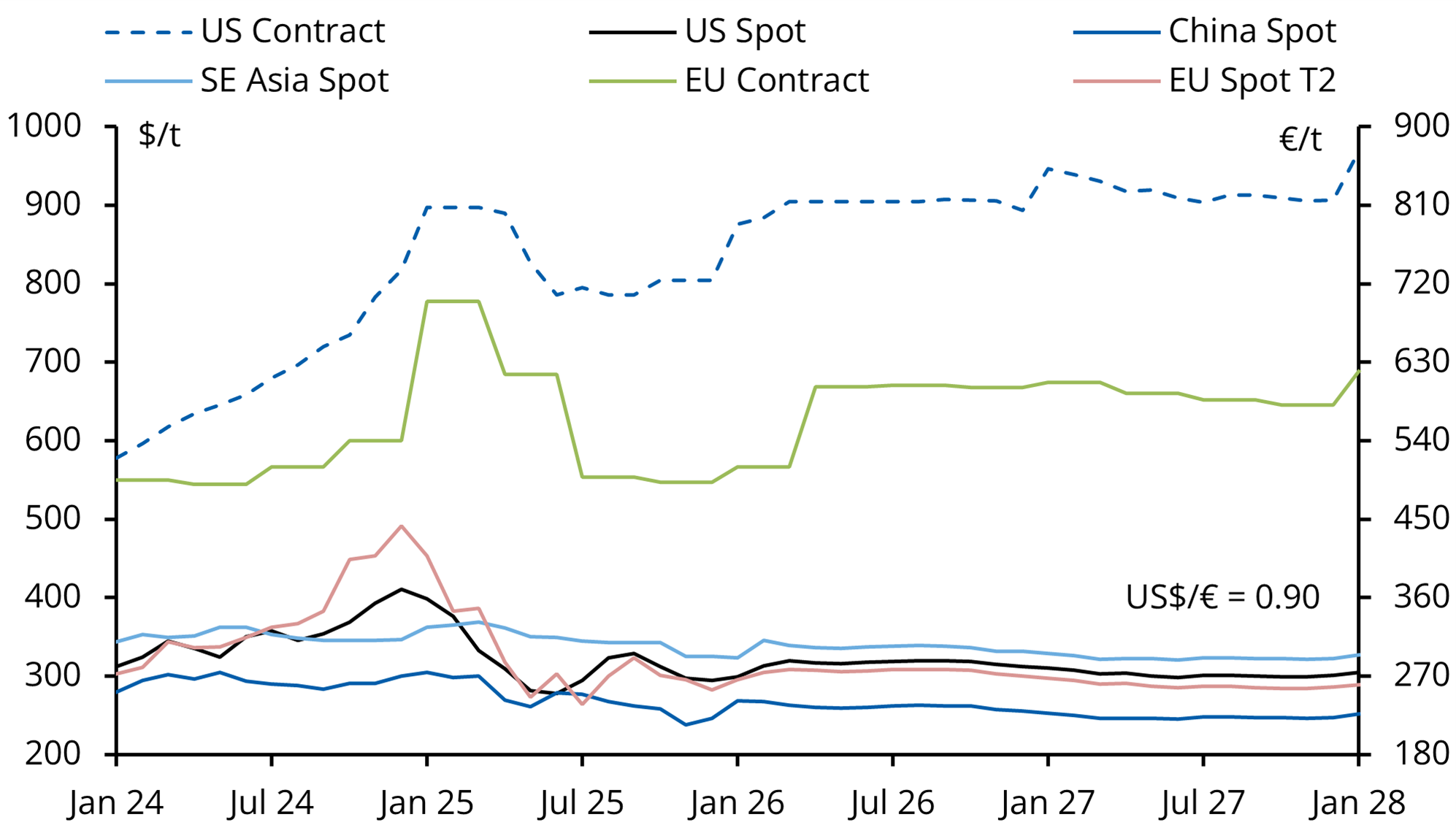

Conventional methanol pricing – 24 months outlook

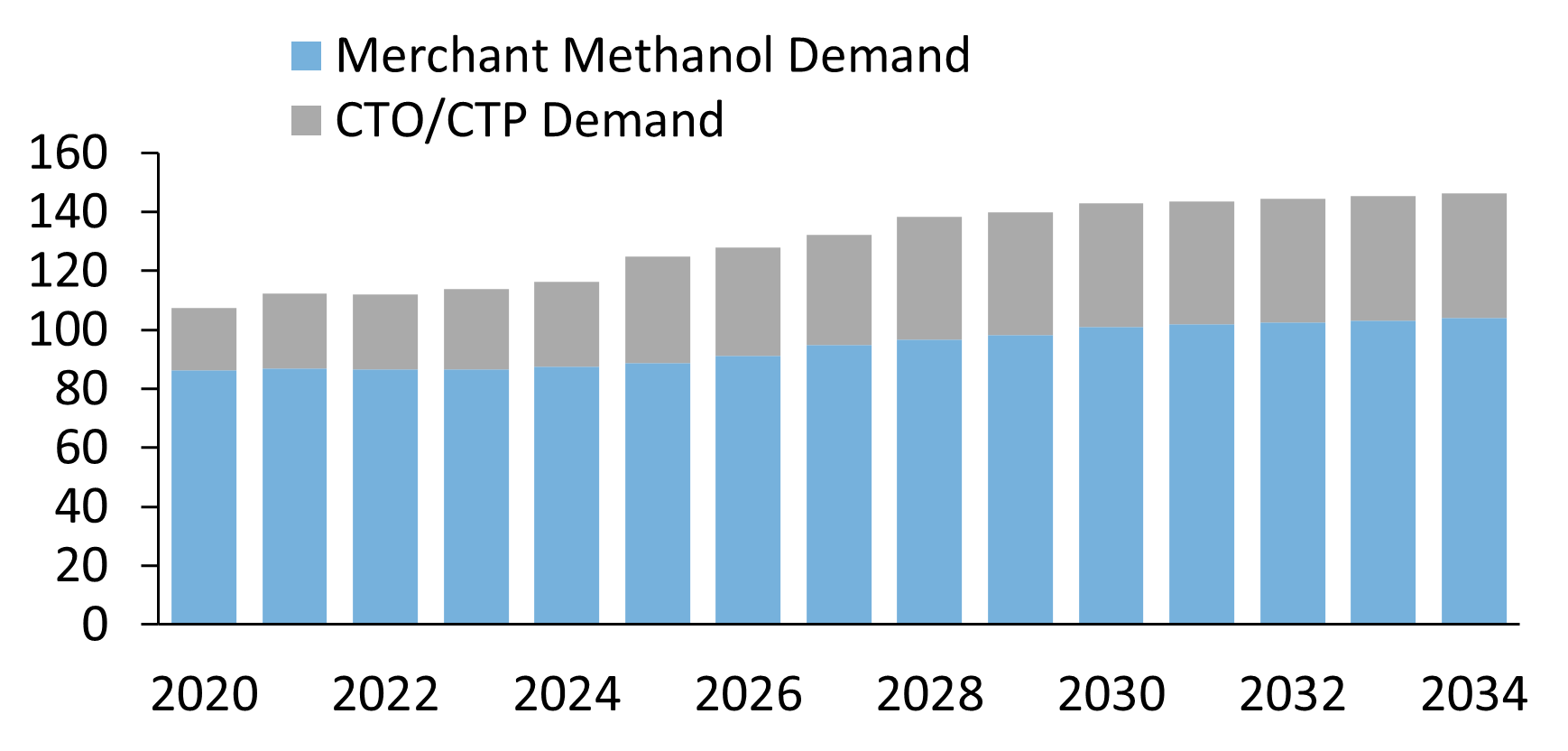

Global methanol industry demand, ‘000 t

While methanol demand growth from 2020 to 2025 averaged under 1pc, we expect average annual growth rates of 2.5-3.0pc per year to return in the forecast period. The growth is expected to include only a small amount of methanol bunker demand from the fossil-based methanol sector.

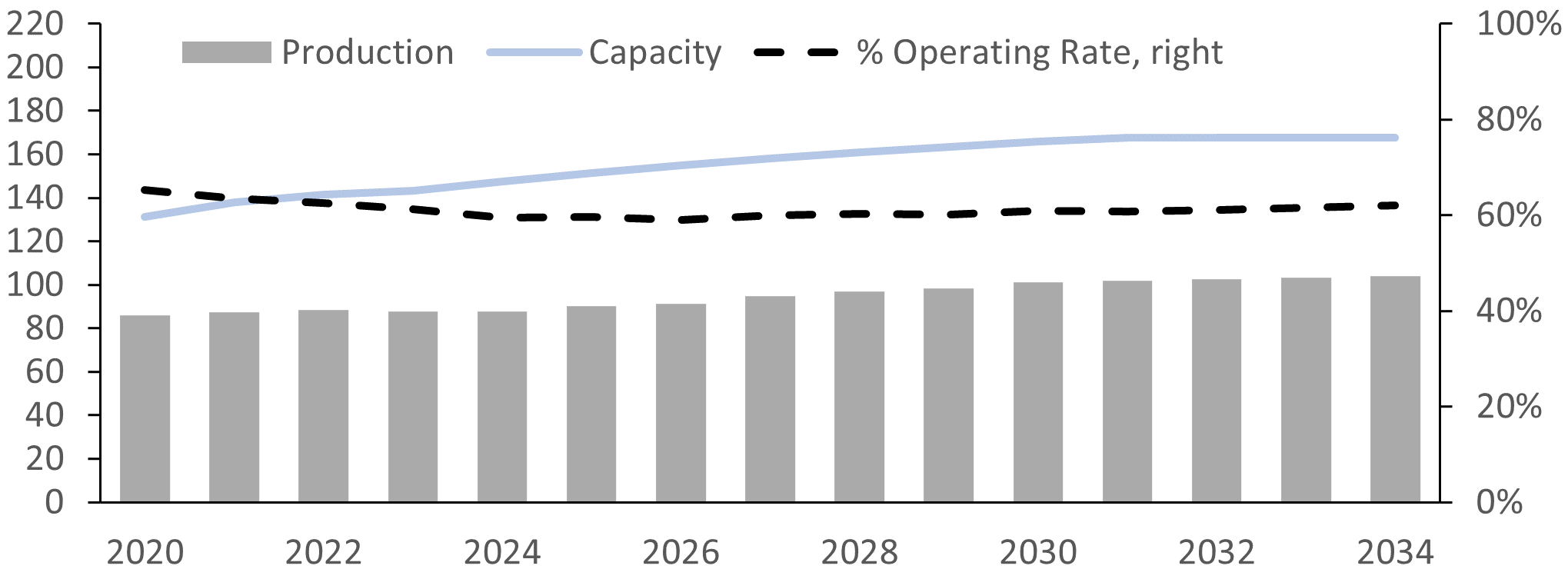

Global methanol production

Reduced demand has slowed expansion plans for some, but operating rates are expected to remain mostly unchanged.

Although the numbers show significant oversupply, the industry typically operates in a balanced way, meaning supply upsets can and will continue to drive price volatility. Non-China methanol capacity tends to run very well and at high rates, while China capacity—the industry’s highest cost of production capacity—runs at reduced rates, absorbing excess supplies from the rest of the world.

With industry capacity outpacing demand growth, this imbalance may limit further price upside for years. China prices will again challenge incremental, high-cost producers, forcing reduced rates or shutdown to bring the industry into balance.

Most new capacity is expected from North America, now Russia, the Middle East and China through the forecast period.